UAE businesses with revenue of AED 50 million or more must appoint an Accredited Service Provider (ASP) by 30 October 2026 and issue e-invoices from 1 January 2027. Businesses below AED 50 million must appoint by 31 March 2027 and go live 1 July 2027. Non-compliance carries a penalty of AED 5,000 per month.

Key facts: UAE e-invoicing at a glance

- Wave 1 (revenue ≥ AED 50M): appoint ASP by 30 October 2026, live 1 January 2027

- Wave 2 (revenue < AED 50M): appoint ASP by 31 March 2027, live 1 July 2027

- Government entities: live 1 October 2027

- Penalty: AED 5,000 per month (Cabinet Decision 106 of 2025)

- Voluntary pilot: open since 1 July 2026; participants penalty-exempt

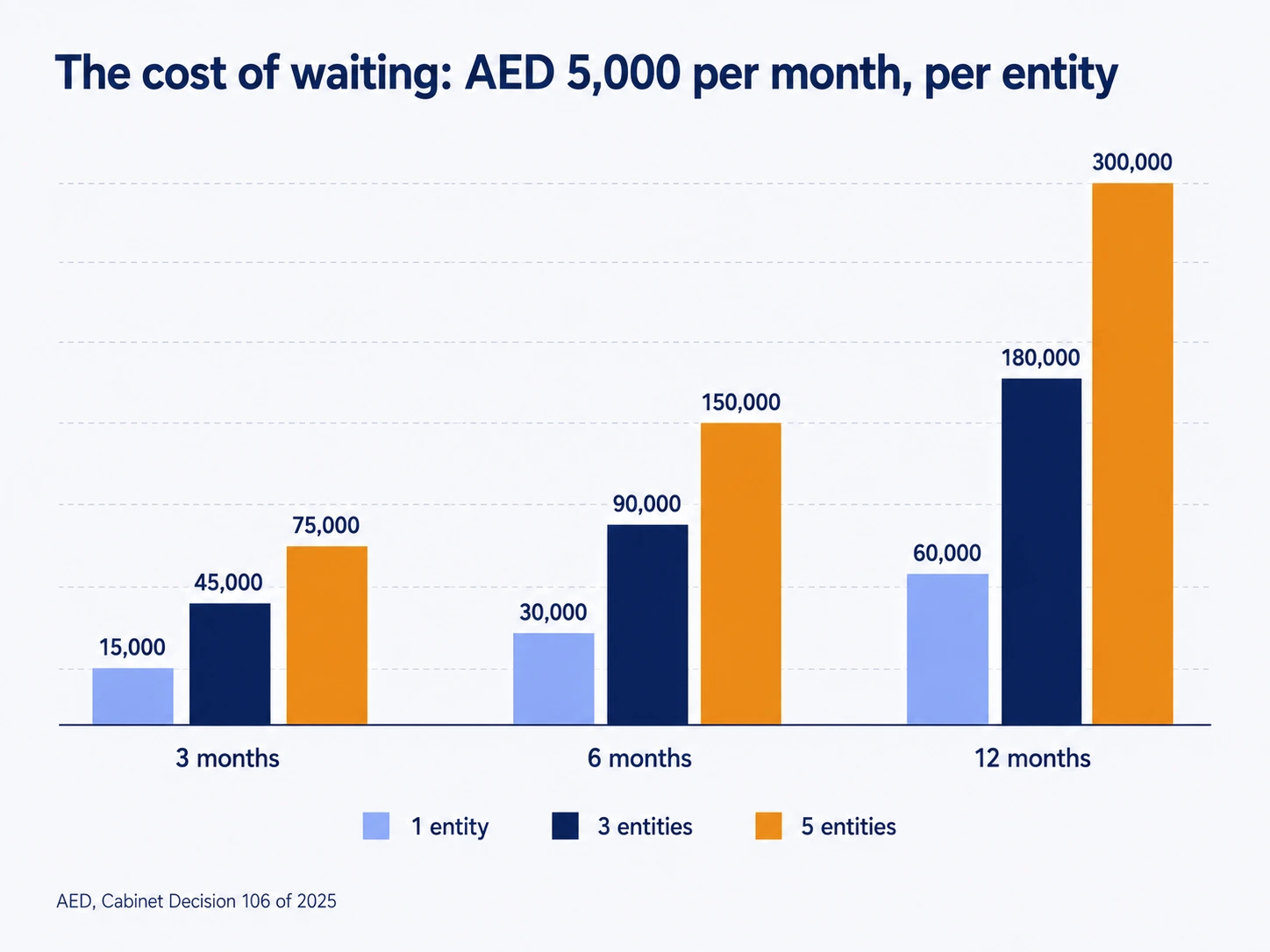

Every month past its UAE e-invoicing deadline now costs a business AED 5,000 — per entity, recurring until it complies. For a five-entity group, a six-month delay is an AED 150,000 line item that buys nothing.

The countdown is no longer theoretical. The voluntary pilot went live on 1 July 2026, and the first mandatory milestone — the Wave 1 deadline to appoint an accredited service provider — falls on 30 October 2026, and the go-live date behind it, 1 January 2027, sits inside year-end close. Yet most guidance available to CFOs and finance directors is written by the very providers competing to be appointed, which makes it selling material, not planning material.

This guide is the neutral version. It covers every deadline in one table, the AED 50 million test that decides which wave you are in, the full penalty math under Cabinet Decision 106 of 2025, and the integration sequence between signing an ASP contract and actually going live.

What Is the UAE E-Invoicing Mandate?

The UAE e-invoicing mandate requires businesses to exchange structured electronic invoices in the PINT AE format through accredited service providers over the Peppol network, with invoice data reported to the Federal Tax Authority. It replaces PDF and paper invoicing for business-to-business and business-to-government transactions, phased in from 2026 to 2027.

The change is more fundamental than it first appears. A PDF attached to an email is a picture of an invoice; a PINT AE e-invoice is machine-readable data that travels system-to-system, is validated before delivery, and is reported to the tax authority as it moves. Invoices that fail validation do not reach the customer.

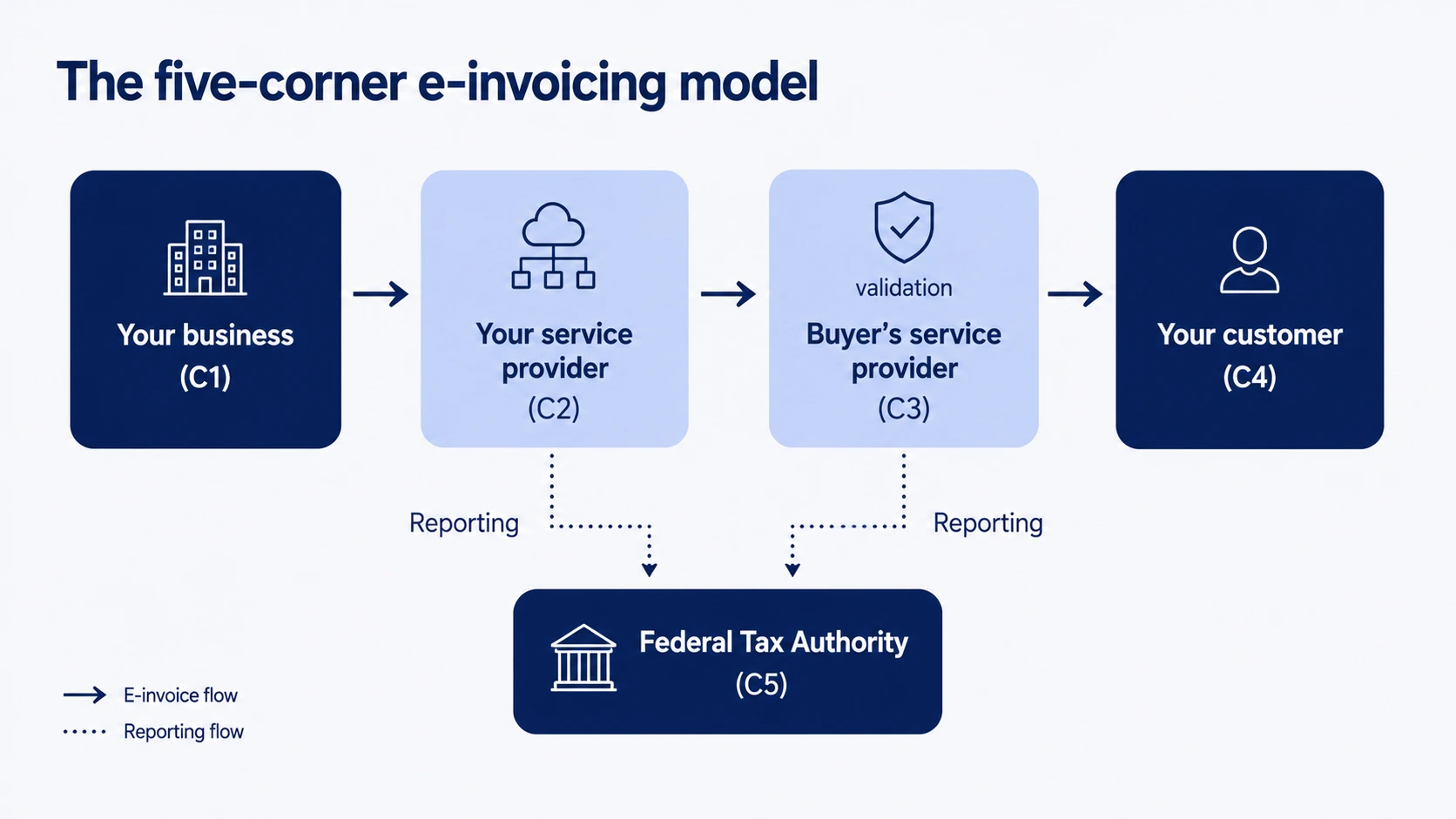

The mechanism is the five-corner model:

- Corner one — your business creates the invoice in your ERP or billing system.

- Corner two — your Accredited Service Provider converts it to PINT AE and transmits it over the Peppol network.

- Corner three — your customer's service provider collects and validates it. If validation fails, the invoice halts here: no tax data is reported, and the rejection is confirmed electronically to your ASP and the FTA.

- Corner four — your customer receives the validated invoice directly into their system.

- Corner five — the Federal Tax Authority receives the reported tax data for every validated invoice.

The legal framework sits with the Ministry of Finance and the Federal Tax Authority, with penalties set out in Cabinet Decision 106 of 2025. The scope covers B2B and B2G transactions, with government entities themselves joining from 1 October 2027. The MoF maintains a public register of pre-approved e-invoicing service providers, which lists 42 providers as of July 2026; pre-approval is granted under Ministerial Decision 64 of 2025, with final accreditation to follow under the same decision.

The UAE is not experimenting alone here. Peppol-based e-invoicing models are already operating in markets from Singapore to Belgium (Peppol country profiles), and the direction of travel for tax administration globally is the same.

Understanding what the mandate is matters less, in practice, than knowing when it applies to you — so let us get the dates on the table.

What Are the UAE E-Invoicing Deadlines for 2026 and 2027?

There are three UAE e-invoicing deadlines. Businesses with revenue of AED 50 million or more must appoint an ASP by 30 October 2026 and go live on 1 January 2027. Businesses under AED 50 million must appoint by 31 March 2027 and go live 1 July 2027. Government entities follow from 1 October 2027.

Each wave carries two distinct obligations. Appointing an ASP is a formal engagement — selecting and contracting an accredited provider by the deadline. Going live means your ERP is actually issuing compliant PINT AE invoices through that provider. The first is paperwork; the second is a systems project, and it is where the time goes.

The Wave 1 appointment deadline was originally 31 July 2026. The Ministry of Finance extended it to 30 October 2026 in response to market readiness. It would be a mistake to read that extension as a pattern: the go-live dates did not move, and no further extensions have been announced.

For Wave 1, the calendar is unforgiving in another way. A 1 January 2027 go-live puts final testing and cutover in December — squarely inside year-end close, audit preparation and, for many IT teams, a change-freeze window. Businesses that leave integration to Q4 will be doing their most delicate systems work at the worst possible time of year.

One definitional point needs care: "revenue" for the AED 50 million test means the gross income earned by a Person during its most recent accounting period, based on financial statements prepared under UAE legislation. Newly established companies use projected revenue for the ongoing financial year, and the test applies to each juridical entity individually — not the consolidated group. That brings us to the question every reader should answer first: which wave are you actually in?

Which Deadline Applies to Your Business?

Your UAE e-invoicing deadline depends on annual revenue. At or above AED 50 million, you are in Wave 1: appoint an ASP by 30 October 2026 and go live 1 January 2027. Below AED 50 million, you are in Wave 2: appoint by 31 March 2027 and go live 1 July 2027.

For a single-entity business with revenue clearly on one side of the line, the test is simple. The complications arrive with structure — and in manufacturing, wholesale and construction, structure is the norm rather than the exception.

Groups with entities of mixed sizes should not assume a single date. The legislation treats each member of a Tax Group as an individual Person for e-invoicing purposes: each member is assessed against the threshold separately and must onboard individually using its own 10-digit Tax Identification Number (TIN), not the Tax Group representative's TRN. Even intra-group transactions between members of the same VAT group are within scope.

Free zone entities are fully in scope, on the same AED 50 million threshold. E-invoicing applies to any Person conducting business in the UAE, regardless of VAT registration status or whether the entity is established on the mainland or in a free zone. One scenario needs attention: where the customer is a free zone entity but the ultimate beneficiary of the supply is a different party, the e-invoice must capture the beneficiary's details.

Businesses hovering near AED 50 million face a practical rather than legal question. If revenue could cross the threshold, the prudent course is to plan on Wave 1 timelines. The cost of preparing early is a few months of lead time; the cost of discovering in November that you were Wave 1 all along is a compressed integration project executed at rush prices.

Multi-entity groups have a planning advantage if they use it: sequence the rollout. Take the largest or most complex entity through first, absorb the lessons, and templatise the work for the rest. What is at stake if an entity misses its date is the subject of the next section — the penalty regime.

What Are the UAE E-Invoicing Penalties for Non-Compliance?

Under Cabinet Decision 106 of 2025, UAE e-invoicing penalties amount to AED 5,000 per month of non-compliance, recurring until the business complies. The penalty applies per non-compliant entity. Businesses participating in the voluntary pilot phase are exempt from penalties while they test.

The headline number sounds manageable until it is multiplied out. The fine recurs monthly and compounds across a group structure:

E-invoicing obligations attach to each Person — every natural or juridical entity — individually, so exposure accumulates per entity rather than being capped at group level.

Even so, for most CFOs the fine is not the largest number in this calculation. E-invoices that fail validation do not reach the customer, and an invoice that never arrives is an invoice that is never paid. Picture a mid-size wholesaler issuing several thousand invoices a month: even a modest rejection rate translates directly into stretched days sales outstanding (DSO) and a working capital problem.

There is also a commercial exposure that no penalty schedule captures. As large buyers and government entities go live, they will expect suppliers to invoice them over the network. A contractor that cannot issue a compliant progress claim to a Wave 1 main contractor is not facing a fine — it is facing exclusion from the payment cycle.

Not sure which of these dates and numbers apply to you? A 30-minute gap analysis answers it.

The penalty regime does contain one deliberate incentive: pilot participants are exempt while they test. That makes the period before your mandatory date a legally sanctioned rehearsal window — a point we return to in the timeline section. First, though, the obligation everyone must complete: appointing an ASP, and what that actually involves.

What Does 'Appointing an ASP' Actually Involve?

Appointing an ASP means formally engaging an accredited service provider from the Ministry of Finance register to transmit your e-invoices over the Peppol network. It involves selecting a provider, contracting, and then integrating your ERP or billing system with that provider — and the integration is usually the longer task.

The most common misunderstanding in the market is that a signed ASP contract equals compliance. It does not. Appointment satisfies the first deadline; compliance at go-live requires your ERP to produce complete, valid PINT AE invoices and exchange them through the ASP. Between contract and compliance sits field mapping, connector development, testing and a parallel run.

Selecting the ASP itself deserves more rigour than it usually gets. The providers on the MoF register differ meaningfully on pricing models (per-invoice versus subscription), pre-built ERP connectors, service level agreements, data residency and support arrangements. The right answer depends on your invoice volumes, your ERP landscape and your entity structure — not on whose advertisement you saw first.

That is a question ASPs themselves cannot answer objectively, because every ASP-authored guide concludes that the answer is them. For transparency: Foxedg is not an ASP and holds no accreditation. We advise businesses on ASP selection — including pre-approved partners Taxilla and Cygnet, whom we disclose when recommending — and we build and manage the ERP-to-ASP connection. Our interest is that the integration works, whichever accredited provider sits on the other end.

Plan the whole sequence backward from your go-live date. Connector build and testing typically run 15 to 60 days depending on the ERP and the size of the business; where a ready-made connector exists — Odoo is one example — integration can complete in as little as a week, or up to 30 days for larger businesses. For the sectors this guide serves, those billing scenarios are precisely where the complexity lives — as the next section sets out.

How Should Manufacturers, Wholesalers, and Contractors Prepare?

High-volume B2B sectors face the heaviest e-invoicing lift. Manufacturers and wholesalers must handle large invoice volumes, credit notes and existing electronic data interchange (EDI) flows; contractors must map progress billing, retention and advance payments to the PINT AE structure. Preparation starts with an invoice-flow inventory across every entity and billing scenario.

For manufacturers and wholesalers, the challenge is volume and data quality. Structured invoicing validates every field on every document, so master-data problems that a human customer would overlook — missing TRNs, inconsistent item codes, incomplete customer records — become automatic rejections at scale. Businesses running EDI with major customers also need clarity on how those flows coexist with Peppol exchange, because the mandate does not switch off existing arrangements overnight.

Construction has a different problem: document complexity. PINT AE defines a specific treatment for each of the sector's billing scenarios, and the mapping is precise rather than intuitive:

- Milestone and instalment billing falls under the continuous-supply scenario.

- Retention must not appear on the e-invoice at all. The invoice shows the net amount payable after the retention adjustment; the retention calculation moves to a separate commercial document, and a separate electronic tax invoice — with applicable VAT — is issued when the buyer becomes liable to release the retained amount.

- Advance payments require a tax invoice at the time of receipt, with the final invoice covering only the remaining balance and referencing the advance in the Preceding Invoice Reference field.

- Sector-specific charges, such as the Dubai Municipality surcharge on construction projects, are reported under Document Level Charges.

A contractor's gap analysis should inventory every billing scenario on live projects, not just the standard invoice.

Both profiles share a structural feature: multiple entities, branches and joint arrangements, each of which needs its own assessment against the threshold and its own connection plan. This is where sequencing the rollout across the group, discussed earlier, pays for itself.

For IT directors and ERP managers, the practical constraints are calendar ones — testing capacity, integration freeze windows, and for Wave 1 the collision between cutover and year-end close. The way to manage all of it is to work backward from the go-live date, which is exactly what the final section does.

How Do You Meet the UAE E-Invoicing Deadline? A Backward Timeline

To meet a UAE e-invoicing deadline, work backward from go-live: run a gap analysis, shortlist and appoint an ASP, build and test the ERP integration, then run parallel invoicing before cutover. For Wave 1 businesses facing a 1 January 2027 go-live, that sequence should already be underway.

The five steps in order. First, a gap analysis: inventory your entities, systems, invoice types and data quality against PINT AE requirements. Second, ASP selection and appointment against criteria that fit your volumes and ERP landscape. Third, connector build — the work that makes your ERP speak PINT AE. Fourth, testing and a parallel run alongside your existing invoicing. Fifth, cutover.

For Wave 1, the backward plan is tight: appointment complete by 30 October, connector build through November, testing and parallel run in December — inside year-end close — and live invoicing on 1 January 2027. Every week of delay now is borrowed from the testing window, which is the one phase you least want to compress.

Wave 2 businesses hold the better hand — and waiting squanders it. The pilot exemption means an SME can connect and test now, penalty-free, while integration capacity is available . When Wave 2 demand converges on the same providers and integrators in early 2027, lead times and pricing will move the way they did in Saudi Arabia's ZATCA rollout — where industry estimates put standard ERP integration at SAR 60,000–180,000 and complex multi-system enterprise setups above SAR 500,000, and vendors report that businesses rushing mandatory sandbox testing to meet a deadline faced longer deployments, failed API calls and higher rework costs. The advantage is not avoiding a fine; it is buying the same project at unhurried prices.

Wherever you sit, the sequence starts in the same place: knowing your gap. A structured gap analysis tells you which wave you are in, what your systems are missing, and how long your version of this project actually takes — before any of it is urgent.

Frequently Asked Questions

Is e-invoicing mandatory in the UAE in 2026?

Not yet for most businesses. The voluntary pilot opened on 1 July 2026. The first mandatory obligation is the Wave 1 ASP appointment deadline of 30 October 2026; the first mandatory go-live is 1 January 2027 for businesses with revenue of AED 50 million or more.

What are the UAE e-invoicing penalties for non-compliance?

AED 5,000 per month under Cabinet Decision 106 of 2025, recurring until the business complies, and applying per non-compliant entity. Businesses participating in the voluntary pilot are exempt during the pilot phase.

Was the UAE e-invoicing deadline extended?

Yes. The Ministry of Finance extended the Wave 1 ASP appointment deadline from 31 July 2026 to 30 October 2026. The go-live dates of 1 January 2027 (Wave 1) and 1 July 2027 (Wave 2) did not change, and no further extensions have been announced.

Does UAE e-invoicing apply to businesses under AED 50 million revenue?

Yes, as Wave 2. These businesses must appoint an accredited ASP by 31 March 2027 and issue e-invoices from 1 July 2027. They may also adopt early through the pilot, penalty-free.

What is an ASP and do I have to use one?

An Accredited Service Provider is a company approved by the Ministry of Finance to transmit e-invoices over the Peppol network and report data to the FTA. Yes — every in-scope business must appoint one from the official register.

Can my current ERP handle UAE e-invoicing?

Most ERPs need a connector or middleware to produce PINT AE invoices and exchange them with an ASP; native support varies by system and version. A gap analysis against your specific ERP, customisations and invoice types answers this definitively.

What is the difference between appointing an ASP and going live?

Appointment is the formal engagement of an accredited provider by the deadline. Going live is when compliant e-invoices actually flow from your ERP through that provider. The integration work between the two is the critical path.

Do free zone companies need to comply with UAE e-invoicing?

Yes, fully. E-invoicing applies to any Person conducting business in the UAE, regardless of VAT registration status or mainland versus free zone establishment, and the same AED 50 million threshold determines the wave. Where the customer is a free zone entity but the ultimate beneficiary of the supply differs, the invoice must capture the beneficiary's details.

The Deadlines Are Fixed. Your Timeline Is Not — Yet.

Three things are worth carrying out of this guide. The UAE e-invoicing deadline that applies to you is fixed by revenue: appoint by 30 October 2026 or 31 March 2027, go live 1 January or 1 July 2027. UAE e-invoicing penalties — AED 5,000 per month — are the floor of the cost of inaction, not the ceiling; rejected invoices and supplier exclusion cost more. And appointment without integration is not compliance: the ERP-to-ASP build is where deadlines are really met or missed.

Businesses that treat the current window as a rehearsal will barely notice their go-live date. Those that wait will buy the same project later, at rush prices, in less time.

If you want to know exactly where you stand against your deadline, book a free 30-minute e-invoicing gap analysis. It maps your entities, systems and invoice flows against your wave's dates — no platform pitch, because we do not have a platform to pitch. You can also download the UAE E-Invoicing Readiness Checklist to run the first pass yourself.

Foxedg is a vendor-neutral e-invoicing integration partner. We are not an ASP. We help UAE businesses select an accredited service provider and build and manage the ERP-to-ASP connection.